The roofing and insurance industry is forever changing, but one thing remains the same.. Storm damage. If you live in an area where storms are more likely, it is important to ensure your home insurance has the proper coverage. So a question that we get asked often is what am I looking for in my policy documents or where do I find that information in my policy?

Generally, home insurance policies are pages upon pages of legal jargon that can be hard to follow and even harder to understand. The declaration page, usually the first page of the policy summarizes the information essential to your insurance coverage. This is where the most important information can be found; deductible, coverage limits, optional coverages, etc.

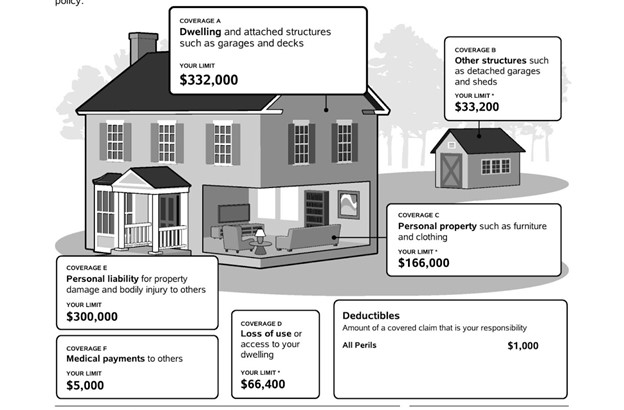

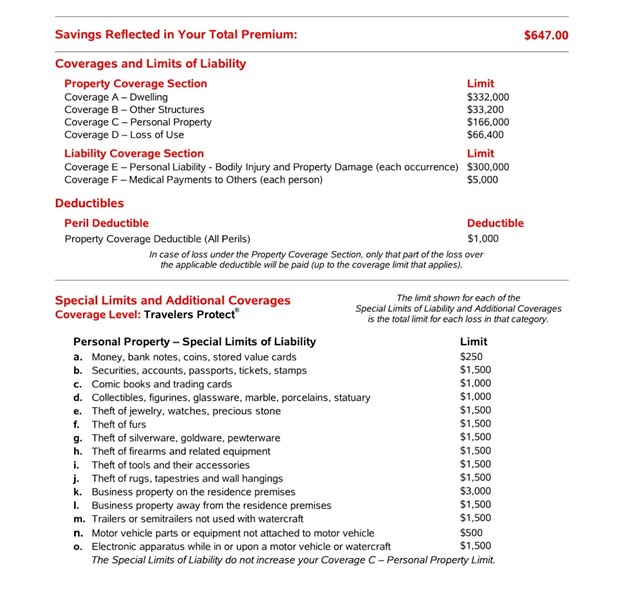

Using the declaration page above – we an determine the following items:

-

The deductible is $1,000.00 no matter the type of loss

-

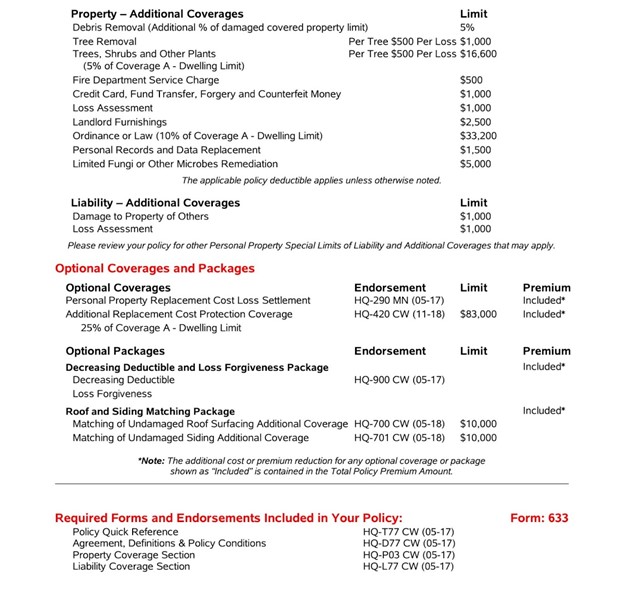

The homeowner has law & ordinance coverage (code coverage)

-

The homeowner has a match endorsement

-

The home is protected up to $332,000 and other structures up to $33,200

While each insurance carrier’s declaration page may look slightly different, all the pertinent information is listed. If you need assistance reading and understanding your policy, reach out to your local agent or any Maven, we would be happy to walk you through it.